Why Seniors Face Home Loan Rejections and How to Overcome Them |

Understanding the Challenges and Exploring Solutions for Older Homeowners |

|

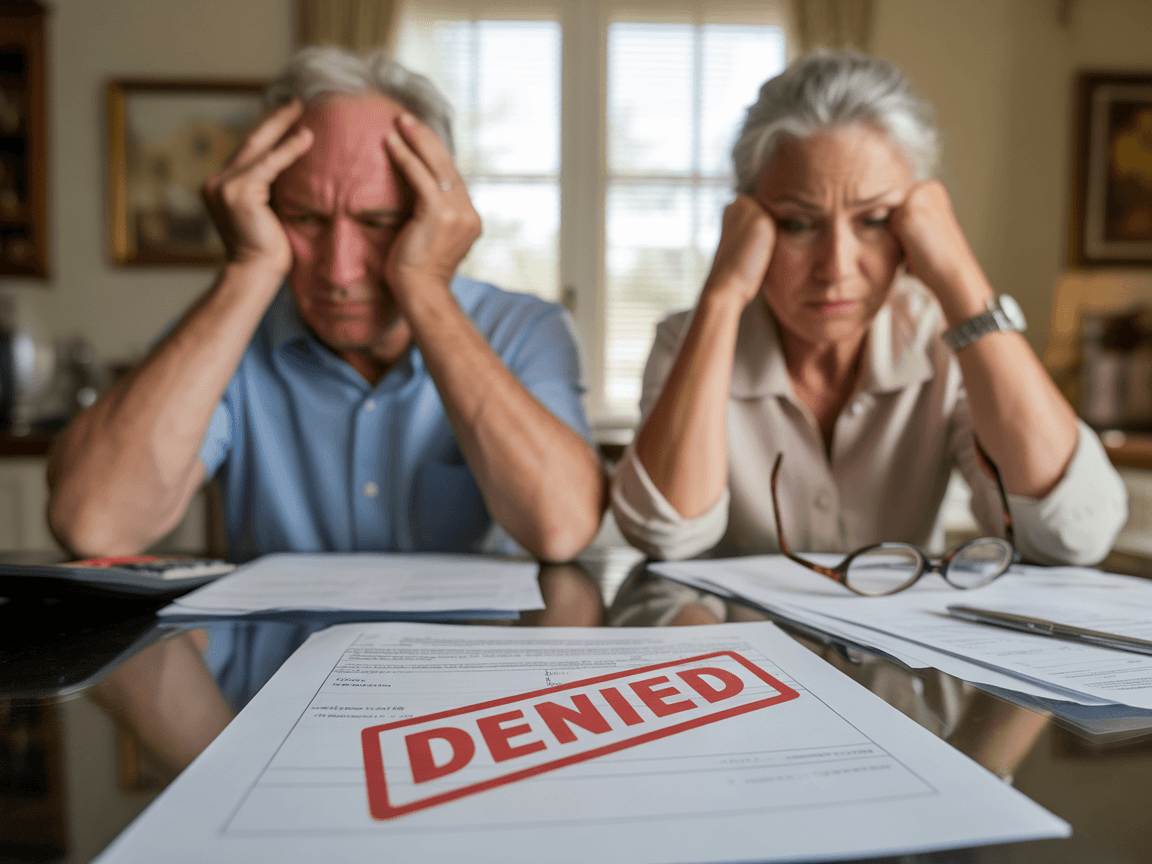

Many seniors assume that a strong credit score and substantial home equity guarantee mortgage approval.

However, numerous older Americans are being denied home equity lines of credit (HELOCs) or cash-out refinances, not due to poor creditworthiness, but because they are retired.

Consider the case of a 60-year-old retired attorney with a credit score exceeding 800 and nearly $400,000 in home equity.

Despite these credentials, her application to refinance for lower payments was denied.

The reason?

Her post-retirement income had decreased, making her a higher risk in the eyes of lenders.

Research from the Federal Reserve Bank of Philadelphia, analyzing over 9 million mortgage applications, found that denial rates rise steadily with age, even after accounting for credit score, property value, and loan type.

Overall refinance rejection rates were 17.5%, but for applicants in their 60s, the rate climbed to 19%, and for those 70 and older, it reached 20%.

Although the Equal Credit Opportunity Act prohibits age discrimination, lenders often assess an older applicant's income, debt-to-income ratio, and mortality risk.

Additionally, concerns about the economic longevity of an older home over the term of the loan, especially for 30-year mortgages, play a role.

The modern mortgage system is optimized for younger, W-2 wage earners, not asset-based underwriting.

This poses a problem when nearly half of older Americans' net worth is tied up in home equity.

With current mortgage rates higher than during the pandemic era and underwriting standards remaining tight, tapping into home equity is becoming increasingly difficult for retirees.

Policy researchers have warned that income-centric underwriting leaves asset-rich, cash-poor seniors with fewer options.

However, there are emerging solutions.

More originators and brokers are offering non-reverse asset-based equity loans, Hi-Tech Lending's Equity Select.

These products require modest payments, appealing to homeowners opposed to increasing debt on their homes.

Now may be the time to reach out to local banks and credit unions to provide viable options for customers who have been denied traditional home equity loans.

By doing so, you can help older homeowners access their housing wealth, offer alternatives to disappointed applicants, and grow your pipeline—a win-win-win situation. |